Why in the news?

Recently, International Centre for Audit of Local Governance (iCAL) was inaugurated in Rajkot, Gujarat.

More on news

- It is the first in country and aims to set global standards for auditing local governance bodies.

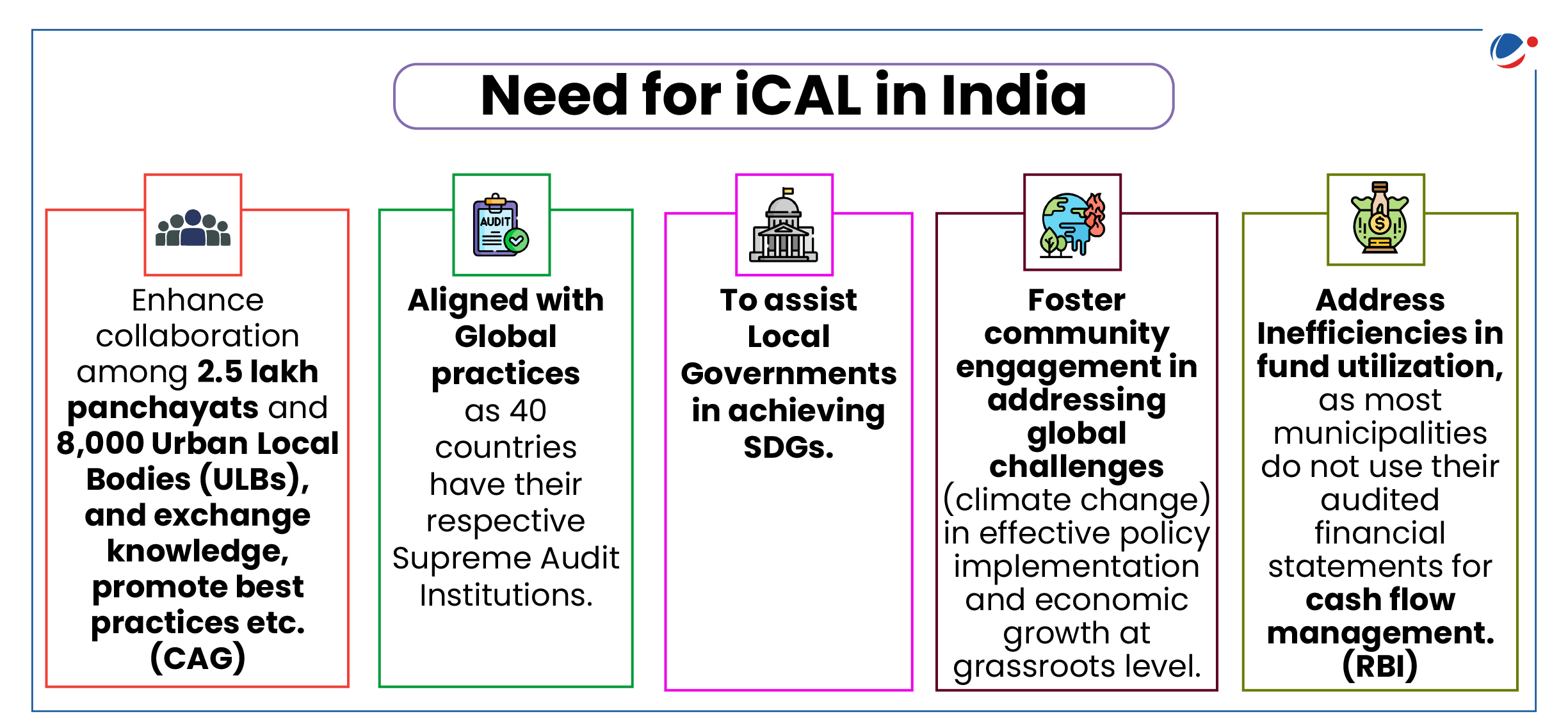

- About iCAL

- It is a collaborative platform for policymakers and auditors and would serve as a centre of excellence for capacity building of auditors.

- It enhances independence of local government auditors to ensure improved financial performance assessment, and service delivery.

- It acts as a knowledge centre and think-tank for addressing governance issues at grassroot levels.

About Local Self Governance and its Audit

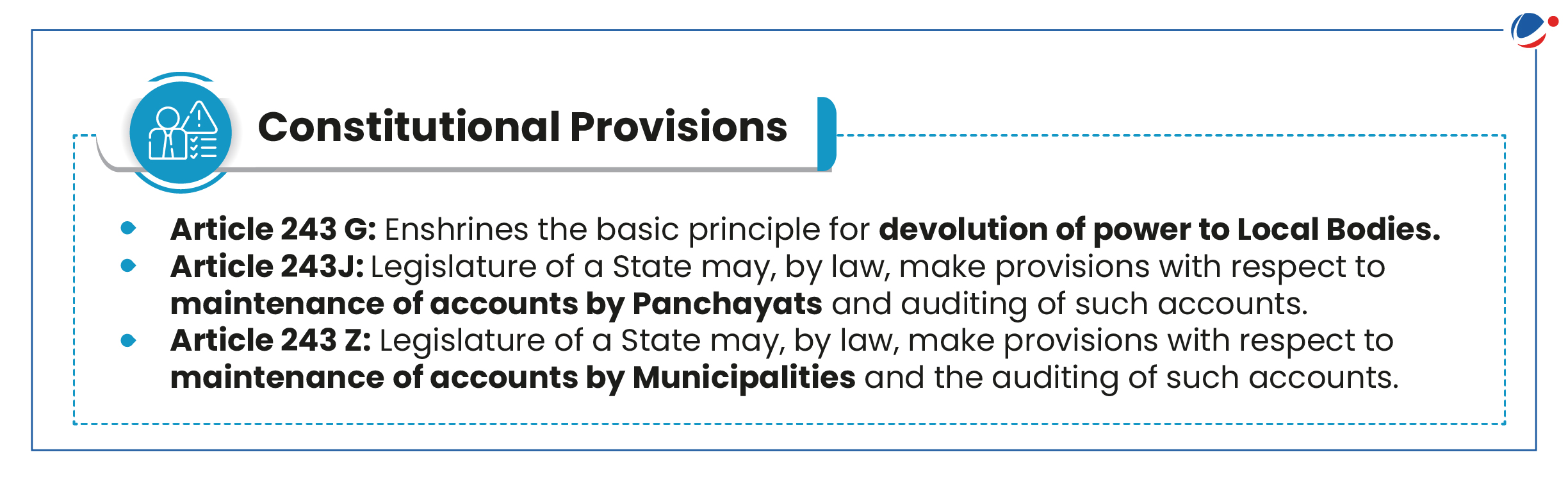

- 73rd and 74th Constitutional Amendment Act, 1992 added Part IX (Eleventh Schedule) and IX-A (Twelfth Schedule) respectively which contains provisions on local self-governance.

- It mandated that State governments constitute panchayats (at village, block and district levels) and municipalities (in form of municipal corporations, municipal councils and nagar panchayats) in every region.

- In 2020, Ministry of Panchayati Raj developed AuditOnline application to conduct online audit of panchayat accounts, ensure accountability in utilisation of funds at ground level.

- It has been awarded the World Summit on Information Society Prizes 2023 at International Telecommunication Union (ITU), Geneva

- Current Auditing Mechanism of Local Bodies

- CAG's mandate for audit of Local Bodies flows from CAG's (Duties, Powers and Conditions of Service) Act, 1971.

- CAG exercises control and supervision over proper maintenance of accounts and auditing for all three levels of Panchayati Raj Institution (PRIs)/Urban Local Bodies (ULBs).

- ELFA/DLFA work under technical guidance and supervision of CAG.

- It is done through Examiner of Local Fund Accounts (ELFA) or Director of Local Fund Accounts (DLFA) in most states. It audits utilization of funds granted by state government to local bodies.

- CAG's mandate for audit of Local Bodies flows from CAG's (Duties, Powers and Conditions of Service) Act, 1971.

Importance of Auditing of Local Bodies

- Financial accountability: Audits safeguard public funds by detecting and preventing fraud, corruption, and financial mismanagement through rigorous scrutiny of expenditures and adherence to financial regulations.

- Performance evaluation: Audits serve as a critical performance evaluation tool for local bodies in examining operations and comparing results against established benchmarks.

- Service delivery: Audit reports findings, recommendation have potential of creating tangible difference in public service delivery, strengthen local bodies and foster grassroots democracy.

- Democratic participation: Auditing activity strengthens governance by increasing citizens engagement e.g. social auditing under Mid-Day Meal Scheme.

- Public trust: Auditors help government organizations achieve accountability and integrity, improve operations, and instil confidence among citizens and stakeholders.

- Decentralisation: Audit observations/findings w.r.t. to status of devolution of functions, funds and functionaries aids in identifying issues, further strengthening decentralisation.

Decentralisation & Inclusive Development

Thus, by empowering local bodies, augmenting their resources, capacity building of functionaries, monitoring and engaging stakeholders such as minorities, civil society organisation etc., local bodies can foster inclusive development. |

Issues associated with Auditing of Local Bodies

- Poor Record Keeping: Many local bodies' financial records are incomplete, inconsistent, and further lack uniform auditing standards across different states and local bodies, leads to variations in the quality of audits.

- Lack of Skilled Personnel: Local bodies often face a shortage of qualified auditors for maintaining accounts. This can lead to inadequate or superficial audits, missing critical issues.

- Overlapping Jurisdictions: The division of auditing responsibilities between different agencies, such as state audit departments, local government auditors, and CAG can create confusion and inefficiencies.

- Out-dated procedures: In many States, the formats and procedures for maintenance of accounts by local bodies were framed decades ago, and are continued without any improvements despite manifold increase in their powers, resources and responsibilities. (Eleventh Finance Commission)

- Low Awareness: General public and local community members often lack awareness of the audit processes and their significance, leading to reduced public scrutiny and accountability.

Way ahead (2nd ARC Recommendations)

- It should be ensured that audit and accounting standards and formats for Panchayats are prepared in a way which is simple and comprehensible to the elected representatives of PRIs.

- The independence of DLFA or any other agency responsible for audit of accounts of local bodies should be institutionalised by making the office independent of the State administration.

- The head of this body should be appointed by State Government from a panel approved by CAG.

- Audit reports on local bodies should be placed before State Legislature and these reports should be discussed by separate committee of State Legislature on the same lines as the Public Accounts Committee.

- Access to relevant information/records to DLFA/designated authority for conducting audit or CAG should be ensured by incorporating suitable provisions in the State Laws governing local bodies.

- Each State may ensure that the local bodies have adequate capacity to match with standards of accounting and auditing.