The Securities and Exchange Board of India (SEBI) has set the ground rules for unregistered financial influencers, or 'finfluencers,' prohibiting regulated entities from dealing with them.

More about News

SEBI decided to introduce a fixed price process for delisting of frequently traded shares and also introduced a delisting framework for Investment and Holding Companies (IHC)

The move comes amid growing concern over the potential risks associated with unregulated finfluencers who might offer biased or misleading advice.

About Financial influencer or 'FinFluencer'

It is a person who gives information and advice to investors on financial topics – usually on stock market trading, personal investments like mutual funds and insurance, primarily on various social media platforms.

Sources of income:

Advertisements- passive income based on number of views.

Collaborations to promote a financial product

Affiliate partnerships: include links in the video description for viewers to buy a product or sign up for a service.

Reasons for rise of finfluencers

Lack of financial literacy: India has a low financial literacy rate of 27%. (National Centre for Financial Education's 2019 survey) andFinfluencers aid in new investor education and awareness creation.

Increased retail investment: The share of retail investors in the cash market turnover jumped from 33% in FY16 to 45 per cent in FY20 and FY21. (National Stock Exchange)

Thus, demand for information relating to financial instruments and stock markets has soared.

Exponential increase in number of new investors: Pandemic provided a boost, with increasing demand and supply for financial advice.

New client registrations hit a record 1.5 million in June 2021, more than double the 0.6 million in June 2020.

Technological advancements: Trading was democratised as new-age broking firms built easy-to-use apps. E.g. Zerodha, Groww.

Affordable smartphones, cheap data plans and digital payments helped finfluencers in reaching the masses through social media platforms.

Issues arising due to rise of Finfluencers

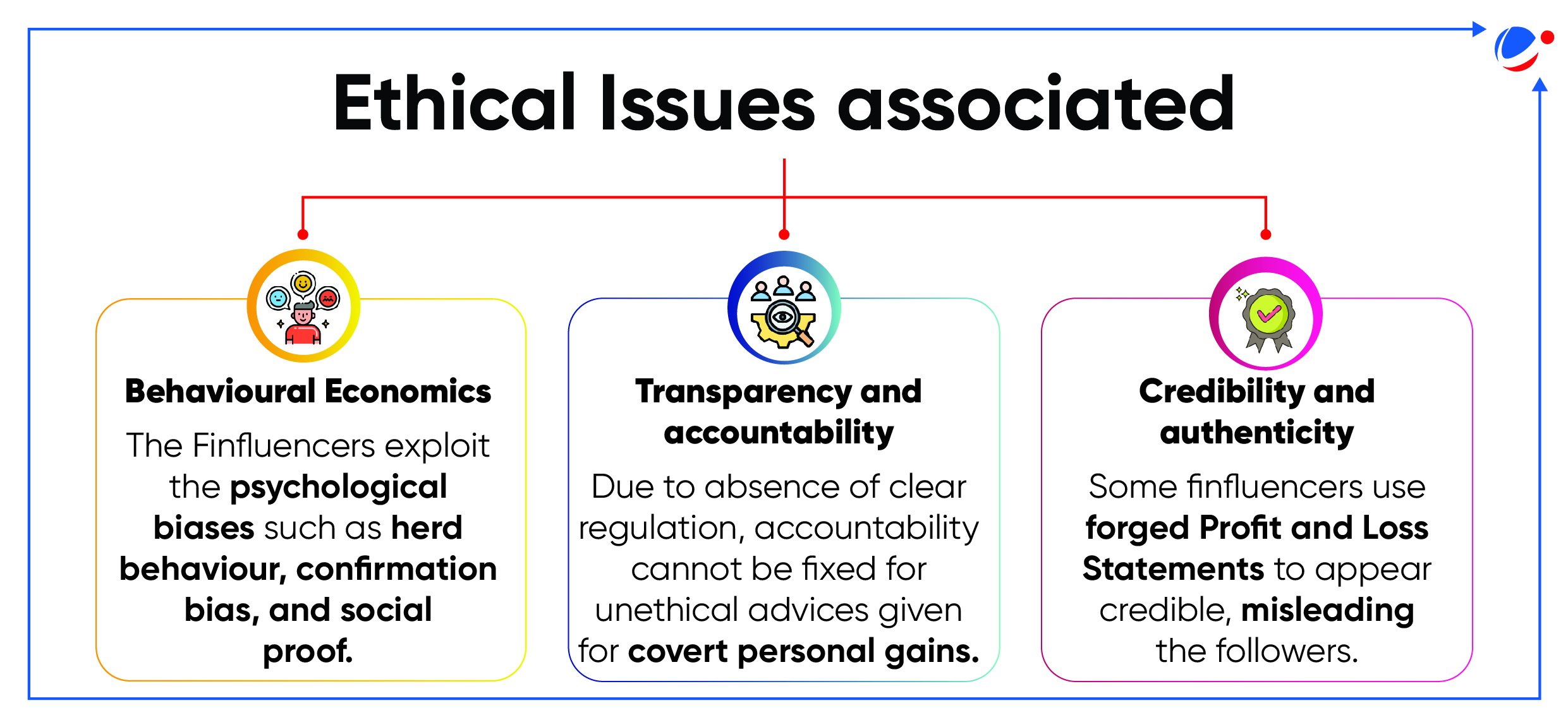

Lack of regulation: Difficult to gauge the expertise and qualification of the finfluencer, fix any liability on the finfluencer or protect an individual from the potential risks.

Market manipulation: Finfluencers are also being paid by the companies to manipulate the stocks for personal gains.

E.g., Salasar Technologies stock prices manipulated by influencers, resulting in huge losses.

High-risk investments: Finfluencers may promote high-risk investment opportunities that promise high returns without providing appropriate risk disclosures.

Views over reliability: The financial advice shared by finfluencers is typically geared towards generating views and likes, rather than providing reliable, well-researched financial information.

This content-first approach compromises the quality and reliability of the advice provided.

Social influence: Finfluencers leverage their social capital and persuasive communication skills to cultivate trust and credibility among their followers, thereby exerting influence over their investment decisions.

Potential for unethical practices: Finfluencers may promote certain stocks in lieu of personal gains through market manipulation, insider trading etc.

Regulatory action taken for Finfluencers

The SEBI (Investment Advisors) Regulations 2013 is a framework for people who give financial advice for a fee.

SEBI Consultation Paperto restrict the association of SEBI registered intermediaries/regulated entities with unregistered 'finfluencers'.

Advertising Standards Council of India (ASCI) revised its guidelines, mandating SEBI registration for influencers.

ASCI and YouTube in-house Rules mandate declaration of the content being paid or promotional to make viewers better informed.

Way Forward

Clear definitions: Of terms like Finfluencers, investment advice etc. so that they stand test of judicial – regulatory scrutiny.

Including coverage of all mediums that have consumer access for financial – investment communication. E.g. TV, Print and digital media.

Improve registration of financial advisors, make mandatory certain disclosure requirements to avoid conflict of interest.

Transparency and data-led communication: Like Real-time digital supervisory mechanism, having a Code of Conduct ensuring the financial information provided is "truthful, balanced, and data-led".

Improved Grievance Redressal Mechanism: This will enable investors report and seek relief for wrong investment advice themselves.

Investor education: Equip investors with knowledge and skills needed to critically appraise digital financial guidance.

Broking firms, mutual funds as well as SEBI have been conducting investor awareness programmes in Tier-II and Tier-III locations.

Self-Regulatory Organizations (SROs): Industry bodies need to initiate self-regulation protocols to uphold their credibility.

Performance Validation Agency (PVA): Establishment of a PVA as a third-party entity to enhance trust and reliability within the financial ecosystem by verifying performance reports.

Global examples of regulation

Australia: Upto 5 years jail for finfluencers providing financial advice without a license.

European Securities and Markets Authority: Defined what constitutes investment recommendations, how to post those advice on social media, and has spelt out penalties for any breach.

New Zealand: Defined code of behavior for finfluencers, tiered mechanism of licensing according to the complexity of advice provided, imposes liability to have content disclaimers require to prominently display risk warnings

Singaporean and Chinese regulators also have Guidelines for Finfluencers.